Qualifying companies

The qualifying criteria for companies have been doubled from April 2026.

Companies must satisfy a number of requirements to qualify to use the EIS and VCT schemes at the time of the share issue and for the following three years.

When the shares are issued, the company must:

- Have gross assets of less than £30m and no more than £35m immediately after the EIS/VCT share issue

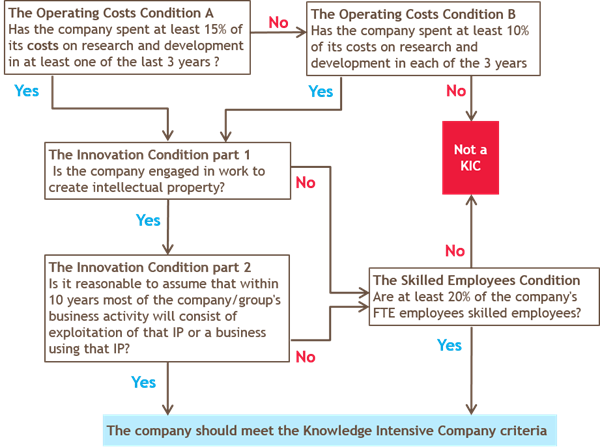

- Have fewer than 500 'full time equivalent' (FTE) employees, or 500 FTE if it is a KIC

- Be unquoted or on AIM, and have no arrangements to become quoted on a recognised stock exchange

- Raise no more than £10m per year per group from a combination of the EIS, SEIS and VCTs (£20m for KICs)

- Raise no more than £24m (£40m if a KIC) in total per group over their lifetime from a combination of the EIS, SEIS and VCTs

- At the time of the share issue and for three years after the share issue, the company must:

- Be independent; not under the control of another company

- Be trading or preparing to trade – though certain types of trade are prohibited. See 'Excluded companies' below

- Having a UK 'permanent establishment', trading mainly in the UK, is no longer a requirement.

There are also anti-avoidance rules to counter pre-arranged exits and any arrangements designed to reduce an investor’s risk.

Finally, all money raised from the issue of EIS and VCT shares must be used to grow and develop the business. It must not be used to make acquisitions of another company’s shares, trade or certain types of trading asset.

Smaller companies may prefer to raise funds via SEIS, rather than EIS or VCT.

Rules for qualifying company

EIS and VCTs are designed to encourage investment in higher risk companies. Companies for which 20% of their trade is in the following activities are excluded from the schemes. These activities that can exclude companies are:

- Dealing in land, shares, futures and other financial instruments

- Dealing in goods other than in the normal course of a retail or wholesale trade

- Banking, insurance, money lending or other financial activities

- Leasing or receiving royalties or license fees, unless the company has created the intangible asset itself

- Providing legal or accountancy services

- Farming, market gardening, woodlands and timber production.

- Property development

- Hotels and nursing homes

- The generation or production of heat, electricity, power, fuel or gas

- Coal and steel production, shipbuilding

- Providing services to a connected party conducting one of the above trades.